Car insurance quotes Washington state are crucial for drivers in the Evergreen State, ensuring compliance with state regulations and providing financial protection in case of accidents. Understanding the various factors that influence insurance premiums, exploring different policy options, and finding affordable coverage are essential for drivers in Washington.

This comprehensive guide will walk you through the intricacies of car insurance in Washington, from mandatory coverage requirements to strategies for obtaining competitive quotes and navigating the claims process. Whether you’re a seasoned driver or a new motorist, this information will empower you to make informed decisions and secure the best car insurance for your needs.

Understanding Washington State Car Insurance Requirements: Car Insurance Quotes Washington State

Driving in Washington State comes with certain responsibilities, and having the right car insurance is one of them. It’s crucial to understand the mandatory insurance coverage types and limits required by the state to ensure you’re legally protected on the road.

Minimum Car Insurance Coverage Requirements

The state of Washington mandates specific car insurance coverage types and minimum limits to ensure financial protection for drivers and their passengers in case of an accident. These minimum requirements are designed to cover the costs of damages to property and injuries to individuals involved in an accident.

- Liability Coverage: This coverage protects you financially if you cause an accident that results in injuries or damages to other people or their property.

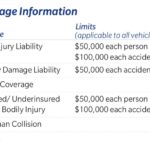

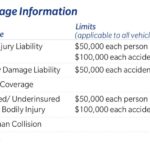

- Bodily Injury Liability: Covers medical expenses, lost wages, and other related costs for injuries sustained by others in an accident you caused. The minimum limit is $25,000 per person and $50,000 per accident.

- Property Damage Liability: Covers damages to other vehicles or property in an accident you caused. The minimum limit is $10,000 per accident.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This coverage protects you if you’re involved in an accident with an uninsured or underinsured driver.

- Uninsured Motorist Coverage (UM): Provides coverage for injuries and damages caused by a driver who does not have insurance. The minimum limit is $25,000 per person and $50,000 per accident.

- Underinsured Motorist Coverage (UIM): Provides coverage for injuries and damages caused by a driver whose insurance limits are insufficient to cover your losses. The minimum limit is $25,000 per person and $50,000 per accident.

Consequences of Driving Without Car Insurance

Driving without the required car insurance in Washington State can have severe consequences, including:

- Fines and Penalties: You could face hefty fines and penalties, including suspension of your driver’s license.

- Legal Liability: If you cause an accident without insurance, you’ll be personally responsible for all damages and injuries, even if you were not at fault.

- Higher Insurance Costs: Once you obtain insurance, you’ll likely face higher premiums due to your previous lapse in coverage.

- Driving Restrictions: You may face driving restrictions or limitations on your ability to operate a vehicle.

Factors Influencing Car Insurance Quotes in Washington

Several factors contribute to the cost of car insurance in Washington State. Insurance companies analyze various aspects of your profile to determine your risk and calculate your premium. Understanding these factors can help you make informed decisions to potentially lower your insurance costs.

Driving History

Your driving history significantly influences your insurance premiums. A clean driving record with no accidents or traffic violations typically results in lower rates. However, insurance companies consider the severity and frequency of accidents and violations. For instance, a DUI conviction or a hit-and-run accident will likely lead to higher premiums compared to a minor fender bender.

In Washington State, insurance companies may consider your driving record for the past three to five years.

Vehicle Type

The type of vehicle you drive is another crucial factor in determining your insurance premiums. Certain car models are known for their safety features, while others are considered more prone to accidents or theft.

- Safety Features: Vehicles equipped with advanced safety features, such as anti-lock brakes, airbags, and stability control, are often associated with lower insurance costs. These features reduce the risk of accidents and injuries, making them more appealing to insurance companies.

- Vehicle Value: The value of your car also impacts your premiums. More expensive cars generally have higher insurance costs due to the potential for greater repair expenses in case of an accident.

- Vehicle Performance: Sports cars and high-performance vehicles are often associated with higher insurance premiums. These vehicles are known for their speed and power, which can increase the risk of accidents and injuries.

Location

The location where you live can significantly impact your car insurance premiums. Factors like population density, crime rates, and traffic congestion influence the likelihood of accidents and theft. Urban areas with high traffic volume and higher crime rates typically have higher insurance premiums compared to rural areas with lower traffic and crime rates.

For instance, living in a densely populated city like Seattle might result in higher insurance costs compared to living in a smaller town in Eastern Washington.

Age

Age is a significant factor in car insurance premiums. Younger drivers, particularly those under 25, are statistically more likely to be involved in accidents. Insurance companies consider this increased risk by charging higher premiums to young drivers. As drivers gain experience and age, their premiums tend to decrease.

This trend reflects the fact that younger drivers have less experience behind the wheel and may be more likely to engage in risky driving behaviors.

Gender

Gender can also influence car insurance premiums, although this factor is becoming less significant in many states. Historically, men have been statistically more likely to be involved in accidents than women. However, this difference is narrowing, and some states have eliminated gender-based pricing.

It is important to note that insurance companies in Washington State are not allowed to use gender as a factor in determining car insurance premiums.

Credit Score, Car insurance quotes washington state

Credit score is an increasingly common factor used by insurance companies to assess risk and determine premiums. A good credit score generally indicates responsible financial behavior, which can be correlated with safer driving habits. Drivers with lower credit scores may be charged higher premiums as they are perceived as higher risk.

Insurance companies may use your credit score as a proxy for your overall risk profile, assuming that individuals with good credit scores are more likely to be responsible and safe drivers.

Obtaining Car Insurance Quotes in Washington

Securing the best car insurance rate in Washington involves comparing quotes from different providers. Thankfully, there are various methods to obtain quotes, each with its advantages and disadvantages.

Online Platforms

Online platforms offer a convenient and efficient way to compare quotes from multiple insurers. They often allow you to enter your information once and receive quotes from various companies simultaneously.

- Advantages: Online platforms are convenient, quick, and allow you to compare quotes from multiple insurers simultaneously. They often offer additional features like personalized recommendations and policy comparisons.

- Disadvantages: Online platforms may not offer access to all insurers, and some companies may not offer their best rates online. Additionally, you may need to provide more personal information online than through other methods.

Brokers

Insurance brokers act as intermediaries between you and insurance companies. They can help you find the best policy for your needs by comparing quotes from multiple insurers.

- Advantages: Brokers can provide personalized advice and help you understand the complexities of insurance policies. They can also handle the entire process of getting quotes and securing coverage.

- Disadvantages: Brokers may charge a fee for their services, and they may not have access to all insurers.

Direct Insurers

Direct insurers sell insurance directly to customers, bypassing brokers or agents. This can offer lower prices as they eliminate the middleman.

- Advantages: Direct insurers often offer lower premiums and more straightforward policies. They also typically have efficient customer service and online tools.

- Disadvantages: Direct insurers may not offer the same level of personalized service as brokers or agents. You may also have fewer options for customization or add-ons.

Tips for Comparing Quotes

- Obtain quotes from multiple insurers: Comparing quotes from different companies is essential to ensure you get the best possible rate. It’s recommended to get quotes from at least three different insurers.

- Provide accurate information: Ensure you provide accurate information to all insurers when obtaining quotes. This includes your driving history, vehicle details, and personal information. Inaccurate information can lead to inaccurate quotes and potential problems later.

- Consider your needs: Before obtaining quotes, think about your specific insurance needs. Factors like your driving history, the type of vehicle you drive, and your coverage preferences will influence the price of your insurance.

- Compare coverage: When comparing quotes, pay attention to the coverage offered by each insurer. Ensure you understand the different types of coverage available and choose a policy that meets your needs.

- Read the fine print: Before making a decision, carefully review the policy documents from each insurer. Pay attention to any exclusions, limitations, or additional fees.

Understanding Common Car Insurance Policies in Washington

Navigating the world of car insurance can feel overwhelming, especially with the variety of policies available. In Washington State, understanding the different types of coverage and their benefits is crucial for making informed decisions that protect you and your vehicle.

Types of Car Insurance Policies in Washington

This table provides a concise overview of common car insurance policies in Washington, outlining their key features, coverage details, and typical premium ranges:

| Policy Type | Coverage Details | Typical Premiums |

|---|---|---|

| Liability Coverage | Covers damages to other people and their property in an accident you cause. This is the most basic requirement in Washington State. | $500 – $1,500 per year |

| Collision Coverage | Covers damages to your vehicle in an accident, regardless of fault. | $200 – $600 per year |

| Comprehensive Coverage | Protects your vehicle from non-accident damages, such as theft, vandalism, fire, or natural disasters. | $100 – $300 per year |

| Uninsured/Underinsured Motorist Coverage (UM/UIM) | Provides coverage if you are involved in an accident with a driver who is uninsured or has insufficient insurance. | $50 – $150 per year |

| Personal Injury Protection (PIP) | Covers medical expenses and lost wages for you and your passengers, regardless of fault. | $100 – $300 per year |

Liability Coverage

Liability coverage is mandatory in Washington State and is essential for protecting yourself financially in case you cause an accident. It covers damages to other people’s property and injuries sustained by others in an accident you are at fault for.

Collision Coverage

Collision coverage protects your vehicle in case of an accident, regardless of who is at fault. This coverage helps pay for repairs or replacement of your vehicle after a collision. It is particularly beneficial for newer vehicles with higher repair costs.

Comprehensive Coverage

Comprehensive coverage offers protection against damages to your vehicle from events other than accidents, such as theft, vandalism, fire, hail, or floods. This coverage is particularly useful for newer vehicles or vehicles with higher value.

Uninsured/Underinsured Motorist Coverage (UM/UIM)

Uninsured/Underinsured Motorist Coverage (UM/UIM) is crucial for protecting yourself in the event of an accident with a driver who does not have insurance or has insufficient coverage. This coverage pays for your injuries and damages if the other driver is unable to cover your losses.

Personal Injury Protection (PIP)

Personal Injury Protection (PIP) coverage is designed to cover your medical expenses and lost wages, regardless of who is at fault in an accident. This coverage can be particularly beneficial for covering medical bills, lost income, and other related expenses.

Finding Affordable Car Insurance in Washington

Securing affordable car insurance in Washington can be a challenge, but it’s not impossible. By understanding your options and taking proactive steps, you can significantly reduce your insurance costs.

Potential Discounts Offered by Insurers

Discounts play a crucial role in lowering your insurance premiums. Insurers in Washington offer various discounts, some of which are:

- Safe Driver Discounts: Maintaining a clean driving record with no accidents or violations is a key factor in securing lower premiums. Many insurers offer discounts for drivers with a good driving history, reflecting their lower risk profile.

- Bundling Policies: Combining multiple insurance policies, such as car, home, or renters insurance, with the same insurer can often result in substantial savings. Insurers often reward policyholders who bundle their coverage, recognizing the loyalty and reduced administrative costs.

- Other Discounts: Insurers may offer additional discounts based on factors like:

- Good Student Discounts: Students with good academic performance may be eligible for discounts, reflecting their responsible nature and lower risk.

- Anti-theft Device Discounts: Installing anti-theft devices in your vehicle, such as alarms or tracking systems, can make it less appealing to thieves and lead to lower premiums.

- Payment Discounts: Paying your premiums annually or semi-annually instead of monthly can sometimes result in a discount, as insurers appreciate the convenience of receiving larger payments.

Negotiating with Insurers and Reducing Overall Insurance Costs

Negotiating with insurers is a valuable strategy for securing a more affordable rate. Here are some tips:

- Shop Around: Obtain quotes from multiple insurers to compare rates and coverage options. This competitive approach allows you to identify the best deals and potentially negotiate a lower price with your preferred insurer.

- Review Your Coverage: Carefully examine your current policy and determine if you can reduce coverage without compromising essential protection. For example, if you have a fully paid-off vehicle, you might consider dropping collision and comprehensive coverage.

- Increase Your Deductible: Raising your deductible, the amount you pay out-of-pocket before your insurance kicks in, can lead to lower premiums. This strategy involves accepting more financial responsibility in the event of an accident but can result in significant cost savings.

- Maintain a Good Driving Record: Driving safely and avoiding accidents or traffic violations is crucial for maintaining a clean driving record. This directly translates into lower premiums, as insurers view drivers with a good history as less risky.

Addressing Car Insurance Claims in Washington

Filing a car insurance claim in Washington State is a process that involves reporting the incident, gathering necessary documentation, and cooperating with your insurance company. The goal is to ensure a smooth and efficient claim process, ultimately leading to fair compensation for your losses.

Filing a Claim

You must promptly notify your insurance company about the accident. It is crucial to report the incident as soon as possible, ideally within 24 hours of the event. This notification can be made by phone, online, or through your insurance agent.

- Provide your insurance company with the details of the accident, including the date, time, location, and a description of what happened.

- Include information about the other parties involved, such as their names, contact information, and insurance details.

- If there are witnesses to the accident, gather their contact information as well.

Documentation

Following the initial report, you will need to provide your insurance company with supporting documentation to substantiate your claim. This documentation helps your insurance company verify the details of the accident and assess the extent of your losses.

- Police Report: If the accident involved injuries or property damage exceeding a certain threshold, a police report is typically required. It serves as an official record of the incident.

- Photographs: Take pictures of the damage to your vehicle, the accident scene, and any injuries sustained. These visuals provide a clear picture of the situation.

- Medical Records: If you have been injured in the accident, you will need to provide your insurance company with your medical records, including bills and treatment summaries.

- Repair Estimates: Obtain repair estimates from reputable auto repair shops for any damage to your vehicle. This documentation provides an assessment of the cost to repair the damage.

Claim Processing and Payment

Once you have filed your claim and provided all necessary documentation, your insurance company will begin the processing phase. The typical timeframe for claim processing can vary depending on the complexity of the claim and the specific insurance company. However, you can generally expect a decision on your claim within a few weeks.

- Review: The insurance company will review your claim, including the accident report, documentation, and any other relevant information.

- Investigation: The insurance company may conduct an investigation to gather further information or verify the details of your claim.

- Negotiation: If the insurance company agrees to cover your claim, they will negotiate a settlement amount with you. This negotiation involves discussing the extent of your losses and the amount of compensation you are entitled to.

- Payment: Once a settlement is reached, the insurance company will issue payment to you. The payment may be made directly to you or to the repair shop or medical provider.

Last Word

Navigating the world of car insurance in Washington can be overwhelming, but with the right knowledge and strategies, you can find affordable and comprehensive coverage that meets your specific needs. By understanding the factors that influence premiums, exploring different policy options, and leveraging available discounts, you can secure the best possible insurance rates while ensuring your financial protection on the road.

FAQ Corner

What are the mandatory car insurance coverages in Washington State?

Washington State requires drivers to have liability coverage, including bodily injury liability, property damage liability, and uninsured/underinsured motorist coverage.

How can I find the best car insurance rates in Washington?

Compare quotes from multiple insurers, consider bundling policies, and explore available discounts. You can use online comparison tools, work with a broker, or contact insurers directly.

What factors influence car insurance premiums in Washington?

Factors include driving history, vehicle type, location, age, gender, credit score, and the amount of coverage you choose.