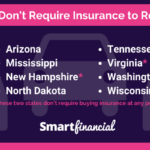

Car insurance different state? It’s a common question for anyone who’s ever moved or is considering relocating. Across the United States, car insurance regulations and costs can vary significantly from state to state, impacting your coverage options, premiums, and overall car insurance expenses. Understanding these differences is crucial to ensure you’re getting the right protection at the best possible price.

This guide delves into the complexities of state-specific car insurance regulations, providing insights into the factors that drive these variations. We’ll explore key coverage differences, compare average premiums across states, and offer tips for navigating the car insurance buying process in different locations. Whether you’re a new driver, a seasoned motorist, or simply seeking to optimize your car insurance, this comprehensive guide will equip you with the knowledge to make informed decisions.

Understanding State-Specific Car Insurance Regulations

Car insurance regulations vary significantly from state to state, creating a complex landscape for drivers to navigate. These differences stem from a combination of factors, including state-specific priorities, risk profiles, and economic considerations.

Factors Influencing State-Specific Car Insurance Requirements, Car insurance different state

State-specific car insurance regulations are influenced by a multitude of factors, each playing a crucial role in shaping the requirements for drivers within a particular jurisdiction. These factors can be broadly categorized into:

- Legislative Priorities: States have varying priorities regarding road safety, consumer protection, and the affordability of car insurance. Some states may prioritize stricter regulations to enhance road safety, while others may focus on ensuring affordable coverage for their residents.

- Risk Profiles: States with higher rates of car accidents, traffic violations, or uninsured drivers may impose stricter insurance requirements to mitigate risks and ensure adequate financial protection for victims.

- Economic Considerations: The cost of living, average income levels, and the availability of insurance providers can influence state-specific regulations. States with higher costs of living may have stricter requirements to ensure sufficient coverage for medical expenses and property damage.

- Political Influences: Political ideologies and lobbying efforts can also influence state-specific car insurance regulations. For instance, states with a strong emphasis on individual liberty may have fewer restrictions on insurance coverage, while states with a more collectivist approach may prioritize mandatory coverage for certain risks.

- Demographic Factors: The age, income, and driving habits of a state’s population can also impact car insurance regulations. States with a higher proportion of young drivers or drivers with a history of accidents may have stricter requirements to mitigate potential risks.

Impact of State-Specific Laws on Coverage Options, Premiums, and Overall Car Insurance Costs

State-specific car insurance regulations have a significant impact on the coverage options available to drivers, the premiums they pay, and the overall cost of car insurance.

- Coverage Options: States have different minimum coverage requirements, which can influence the types of coverage available to drivers. Some states require only liability coverage, while others mandate comprehensive and collision coverage as well. The availability of optional coverages, such as uninsured/underinsured motorist coverage, can also vary by state.

- Premiums: State regulations can affect premiums by influencing factors such as minimum coverage requirements, the availability of discounts, and the use of risk-based pricing models. States with stricter regulations or higher risk profiles may have higher average premiums.

- Overall Car Insurance Costs: The combination of coverage options, premiums, and other factors, such as the availability of insurance providers, can significantly impact the overall cost of car insurance in a particular state. States with stricter regulations, higher risk profiles, or limited competition in the insurance market may have higher overall car insurance costs.

Comparing Car Insurance Rates Across States

Car insurance rates vary significantly from state to state, and understanding these differences can help you find the best deal for your needs. Several factors contribute to these variations, including state laws, traffic density, accident rates, and the cost of car repairs.

Average Car Insurance Premiums by State

The following table presents average annual car insurance premiums for different states, according to a recent study by the Insurance Information Institute (III):

| State | Average Annual Premium |

|---|---|

| Michigan | $2,634 |

| Louisiana | $2,437 |

| Florida | $2,378 |

| New Jersey | $2,274 |

| Texas | $2,139 |

| California | $2,088 |

| Pennsylvania | $1,956 |

| New York | $1,898 |

| Ohio | $1,886 |

| Illinois | $1,825 |

Factors Influencing Car Insurance Premiums

Several factors contribute to the differences in car insurance premiums across states:

- State Laws and Regulations: Different states have varying regulations regarding minimum insurance coverage requirements, which can impact premiums. States with higher minimum coverage requirements may have higher average premiums.

- Traffic Density and Accident Rates: States with high traffic density and frequent accidents tend to have higher insurance premiums. This is because insurers face a higher risk of claims in such areas.

- Cost of Car Repairs: States with higher costs of car repairs and labor may have higher insurance premiums. This is because insurers need to cover the costs of repairs in the event of an accident.

- Demographics and Driving Habits: Factors like age, gender, driving history, and vehicle type can also influence premiums. States with a higher proportion of young drivers or drivers with poor driving records may have higher premiums.

- Competition Among Insurers: The level of competition among insurers in a state can also impact premiums. States with more insurance companies competing for customers may have lower average premiums.

Average Car Insurance Premiums by Car Type

The following table shows average annual car insurance premiums for different car types across various states, based on data from the III:

| State | Sedan | SUV | Truck |

|---|---|---|---|

| Michigan | $2,400 | $2,800 | $3,000 |

| Louisiana | $2,200 | $2,600 | $2,800 |

| Florida | $2,100 | $2,500 | $2,700 |

| New Jersey | $2,000 | $2,400 | $2,600 |

| Texas | $1,900 | $2,300 | $2,500 |

Key Coverage Differences in Car Insurance Policies

Car insurance policies can vary significantly across different states, with each state having its own set of regulations governing the types of coverage required and the optional coverage options available. These differences can have a substantial impact on the cost and scope of your car insurance policy. Understanding these variations is crucial for making informed decisions about your car insurance needs.

Mandatory Coverage Requirements

State laws mandate specific coverage requirements for car insurance policies. These requirements are designed to protect individuals from financial losses resulting from car accidents. The most common mandatory coverages include:

- Liability Coverage: This coverage protects you from financial responsibility if you are at fault in an accident that causes injuries or damage to another person or property. It typically includes bodily injury liability and property damage liability coverage. For instance, a policy with a $100,000/$300,000 liability limit would cover up to $100,000 per person and $300,000 per accident for bodily injury claims, and up to $50,000 per accident for property damage claims.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This coverage protects you in the event of an accident with a driver who is uninsured or has insufficient insurance to cover your losses. It can provide coverage for your injuries and property damage, even if the other driver is at fault.

- Personal Injury Protection (PIP): This coverage, often required in “no-fault” states, pays for your medical expenses and lost wages regardless of who caused the accident. It helps ensure that you receive timely medical care and financial support after an accident, even if you are at fault.

Optional Coverage Options

While mandatory coverages are essential, there are several optional coverage options that can provide additional protection. These options may vary based on state regulations, and your individual needs will determine which ones are right for you. Some common optional coverages include:

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if it is damaged in an accident, regardless of who is at fault.

- Comprehensive Coverage: This coverage protects your vehicle from damage caused by events other than collisions, such as theft, vandalism, hailstorms, or floods.

- Rental Reimbursement Coverage: This coverage provides financial assistance for a rental car while your vehicle is being repaired after an accident.

- Roadside Assistance Coverage: This coverage provides assistance with services such as towing, flat tire changes, and battery jump starts.

- Gap Insurance: This coverage protects you from potential financial loss if your vehicle is totaled and the insurance payout is less than the amount you owe on your loan or lease.

State-Specific Regulations and Coverage Limitations

State-specific regulations can also impact coverage limitations and exclusions. For example, some states may have specific requirements for coverage limits or may exclude certain types of vehicles or drivers from coverage. It’s important to understand the specific regulations in your state and how they may affect your policy.

For example, some states may have specific requirements for coverage limits, such as minimum liability limits or maximum coverage amounts for certain types of losses. Other states may have exclusions for certain types of vehicles, such as motorcycles or recreational vehicles.

Navigating the Car Insurance Buying Process in Different States

Purchasing car insurance can be a complex process, especially when considering state-specific regulations and varying insurance provider offerings. This guide aims to provide a comprehensive understanding of the car insurance buying process in different states, helping you navigate the intricacies and secure the best possible coverage at an affordable rate.

Understanding the Key Steps Involved in Obtaining Car Insurance

The process of obtaining car insurance involves several key steps, which may vary slightly depending on the state.

- Gather Your Information: Begin by collecting essential information, such as your driver’s license details, vehicle information (make, model, year), and any relevant driving history records.

- Research and Compare Insurance Providers: Explore different insurance providers in your state, comparing their coverage options, rates, and customer reviews. Utilize online comparison tools or consult with insurance brokers for a comprehensive overview of available choices.

- Obtain Quotes: Contact the insurance providers you’re interested in and request quotes for your specific needs. Be sure to provide accurate information to ensure accurate rate calculations.

- Review and Choose a Policy: Carefully review the quotes you receive, comparing coverage details, deductibles, and premiums. Choose the policy that best suits your budget and insurance needs.

- Make Payment and Receive Confirmation: Once you’ve selected a policy, make the necessary payment to the insurance provider. You will then receive confirmation of your coverage, including your policy details and effective date.

Comparing Car Insurance Quotes from Different Providers

Comparing car insurance quotes from different providers is crucial for securing the best possible rates.

- Use Online Comparison Tools: Many online comparison websites allow you to enter your information and receive quotes from multiple insurers simultaneously. These tools save time and effort, providing a comprehensive overview of available options.

- Consider Coverage Options: Carefully compare the coverage options offered by each insurer, ensuring they meet your specific needs. Consider factors like liability limits, collision and comprehensive coverage, and uninsured/underinsured motorist coverage.

- Compare Deductibles and Premiums: Pay close attention to the deductibles and premiums associated with each policy. Higher deductibles generally result in lower premiums, while lower deductibles lead to higher premiums. Choose a balance that suits your risk tolerance and budget.

- Review Customer Reviews and Ratings: Check online reviews and ratings of insurance providers to gain insights into their customer service, claims handling, and overall reputation.

Tips on Negotiating Car Insurance Premiums

While negotiating car insurance premiums may seem daunting, several strategies can help you secure better rates.

- Shop Around and Compare Quotes: Regularly compare quotes from different insurers to ensure you’re getting the best possible rates. Don’t hesitate to switch providers if you find a better offer.

- Bundle Your Policies: Consider bundling your car insurance with other policies, such as homeowners or renters insurance, to potentially qualify for discounts.

- Maintain a Good Driving Record: A clean driving record is crucial for securing lower premiums. Avoid traffic violations and accidents to maintain your eligibility for discounts.

- Explore Discounts: Inquire about available discounts, such as safe driver discounts, good student discounts, and multi-car discounts.

- Increase Your Deductible: Consider increasing your deductible to lower your premiums. This strategy can be effective if you’re comfortable assuming a higher financial responsibility in the event of an accident.

Understanding State-Specific Car Insurance Claims Processes

Filing a car insurance claim can be a stressful experience, especially when you’re dealing with the aftermath of an accident. The process can vary significantly from state to state, making it crucial to understand the specific regulations and procedures in your area. This information will help you navigate the claims process efficiently and maximize your chances of a successful claim.

Steps Involved in Filing a Car Insurance Claim

The initial steps in filing a car insurance claim are generally consistent across states, but the specific details and timelines can differ.

- Report the Accident: Immediately contact your insurance company to report the accident, providing details about the date, time, location, and circumstances of the incident. This is often done through a phone call or online portal.

- File a Claim: Your insurance company will guide you through the process of filing a formal claim. This typically involves providing additional information about the accident, including details about the other parties involved and any injuries sustained.

- Provide Documentation: You’ll be required to provide supporting documentation to substantiate your claim. This may include a police report, medical records, photos of the damage, and repair estimates.

- Insurance Company Investigation: The insurance company will investigate the claim to determine liability and assess the extent of the damages. This may involve contacting the other party involved in the accident and conducting an independent inspection of the vehicle.

- Claim Settlement: Once the investigation is complete, the insurance company will make a decision on your claim. This may involve offering a settlement amount, denying the claim, or requiring additional information.

Differences in Claim Processing Times and Procedures

The time it takes to process a car insurance claim can vary significantly across states.

- State Laws and Regulations: State laws and regulations governing insurance claims can impact the speed and efficiency of the claims process. Some states have stricter requirements for documentation or investigation, which can slow down the process.

- Insurance Company Practices: Each insurance company has its own internal processes and procedures for handling claims. Some companies are known for their faster processing times, while others may take longer.

- Complexity of the Claim: Claims involving multiple parties, significant damages, or disputed liability can take longer to process than simpler claims.

- Volume of Claims: States with a high volume of car accidents may experience longer processing times due to the increased workload on insurance companies.

Navigating the Claims Process

Here are some tips for navigating the car insurance claims process:

- Be Prepared: Keep your insurance policy information readily available, including your policy number, coverage limits, and contact information.

- Be Prompt: Report the accident to your insurance company as soon as possible. Delays in reporting can impact your claim.

- Be Cooperative: Cooperate fully with the insurance company’s investigation. Provide all required documentation promptly and truthfully.

- Be Patient: The claims process can take time, especially if the claim is complex. Be patient and follow up with your insurance company if you have any questions or concerns.

- Consider Legal Counsel: If you have a complex claim or you’re not satisfied with the insurance company’s handling of your claim, consider consulting with an attorney.

End of Discussion

Navigating the world of car insurance can be daunting, especially when you factor in the complexities of state-specific regulations. By understanding the factors that influence car insurance rates and coverage options, you can empower yourself to make informed choices. Remember to compare quotes from multiple insurers, consider your individual needs, and prioritize comprehensive coverage to protect yourself and your loved ones on the road.

FAQ Insights: Car Insurance Different State

What are the main reasons for car insurance rate variations across states?

Car insurance rates are influenced by a multitude of factors, including the frequency of accidents, the cost of healthcare, and the density of population in a given state. These factors can significantly impact the risk assessment used by insurance companies to determine premiums.

How can I compare car insurance quotes from different providers in my new state?

Many online comparison tools allow you to input your details and receive quotes from multiple insurers simultaneously. You can also contact insurance agents directly for personalized quotes.

What are some tips for negotiating car insurance premiums?

Consider bundling your car insurance with other policies like homeowners or renters insurance. Improving your driving record and maintaining a good credit score can also help lower your premiums. Don’t hesitate to ask about discounts for safety features in your car or for being a good driver.