Auto insurance requirements in my state are crucial for responsible drivers, ensuring financial protection in case of accidents. Understanding these requirements is essential for complying with state laws and safeguarding yourself from potential financial burdens.

This guide delves into the intricacies of auto insurance, covering everything from mandatory coverage types to factors influencing premiums. We’ll explore the different types of insurance available, the minimum liability limits required, and the consequences of driving without adequate coverage.

Understanding State-Specific Auto Insurance Requirements

Driving a vehicle is a privilege and responsibility that comes with certain legal obligations, including carrying adequate auto insurance. State laws mandate auto insurance to protect drivers, passengers, and other road users from financial hardship in the event of an accident. Understanding these requirements is crucial to ensure you are legally compliant and financially protected.

Penalties for Driving Without Insurance

Driving without the minimum required auto insurance coverage can result in severe consequences, including:

- Fines: State-specific fines can range from hundreds to thousands of dollars.

- License Suspension: Driving privileges may be suspended until insurance is obtained.

- Vehicle Impoundment: Your vehicle may be impounded until insurance is secured.

- Jail Time: In some cases, driving without insurance can lead to jail time, particularly for repeat offenses.

- Higher Insurance Premiums: Once you do obtain insurance, your premiums will likely be significantly higher due to your prior lapse in coverage.

Types of Auto Insurance Coverage

Auto insurance policies typically offer a range of coverage options designed to protect you financially in various situations. Understanding these coverage types is essential to determine the right combination for your needs and budget:

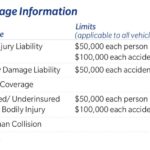

- Liability Coverage: This coverage is mandatory in most states and protects you financially if you cause an accident that results in injuries or property damage to others. It covers the costs of medical expenses, lost wages, and property repairs for the other party involved.

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if it is damaged in an accident, regardless of fault. You can choose a deductible, which is the amount you pay out of pocket before your insurance kicks in.

- Comprehensive Coverage: This coverage protects your vehicle against damage caused by events other than accidents, such as theft, vandalism, fire, or natural disasters. It also includes a deductible.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This coverage protects you if you are injured in an accident caused by a driver who is uninsured or underinsured. It helps cover your medical expenses, lost wages, and other damages.

- Personal Injury Protection (PIP): This coverage pays for your medical expenses, lost wages, and other related costs, regardless of fault, if you are injured in an accident. It is often required in “no-fault” states.

- Medical Payments Coverage (Med Pay): This coverage provides medical expense coverage for you and your passengers, regardless of fault, up to a certain limit.

- Rental Reimbursement: This coverage helps pay for a rental car if your vehicle is damaged and needs repairs.

- Roadside Assistance: This coverage provides assistance with services such as towing, flat tire changes, and jump starts.

Mandatory Coverage in [Your State Name]

[Your State Name] requires all drivers to carry the following minimum auto insurance coverage:

- Liability Coverage: [Your State Name] mandates a minimum of [Your State’s Minimum Liability Coverage Limits] for bodily injury and property damage liability.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): [Your State Name] also requires [Your State’s Minimum UM/UIM Coverage Limits].

Minimum Liability Coverage Requirements

Liability coverage is a crucial aspect of auto insurance, protecting you financially in case you’re responsible for an accident that causes injuries or property damage to others. Understanding your state’s minimum liability coverage requirements is essential to ensure you’re adequately protected and avoid potential financial hardship.

Minimum Liability Coverage Limits

Your state’s minimum liability coverage requirements are the least amount of insurance coverage you’re legally required to carry. These limits specify the maximum amount your insurance company will pay for bodily injury and property damage caused by an accident.

The minimum liability coverage limits vary from state to state. In most states, these limits are expressed in terms of “per person” and “per accident.”

For example, a minimum liability coverage requirement of 25/50/25 means:

* $25,000 per person for bodily injury liability.

* $50,000 per accident for bodily injury liability.

* $25,000 per accident for property damage liability.

Consequences of Insufficient Liability Coverage

If you’re involved in an accident and your liability coverage is insufficient to cover the damages, you’ll be personally responsible for the remaining costs. This could include:

* Medical expenses: If you cause an accident resulting in injuries to others, you’ll be responsible for their medical bills exceeding your liability coverage limits.

* Property damage: If you cause damage to another person’s vehicle or property, you’ll be responsible for the repair or replacement costs exceeding your liability coverage limits.

* Legal fees: If you’re sued by the other party, you’ll be responsible for the legal fees associated with defending yourself in court.

* Wage loss: If you cause an accident that prevents the other party from working, you could be held responsible for their lost wages.

Minimum Liability Coverage Requirements by Vehicle Type

The minimum liability coverage requirements may vary depending on the type of vehicle you drive.

| Vehicle Type | Bodily Injury Liability | Property Damage Liability |

|—|—|—|

| Passenger Cars | $25,000 per person / $50,000 per accident | $25,000 per accident |

| Motorcycles | $25,000 per person / $50,000 per accident | $25,000 per accident |

| Commercial Vehicles | $50,000 per person / $100,000 per accident | $25,000 per accident |

It’s important to note that these are just examples, and actual minimum liability coverage requirements may vary depending on your state and specific vehicle type. Always consult with your insurance agent or review your state’s Department of Motor Vehicles website for accurate and up-to-date information.

Other Required Coverages: Auto Insurance Requirements In My State

In addition to the minimum liability coverage, your state may require other types of auto insurance to ensure comprehensive protection for you and others on the road. These coverages provide financial support in various situations that standard liability insurance might not cover.

Uninsured/Underinsured Motorist Coverage

This coverage protects you and your passengers in case you are involved in an accident with a driver who is uninsured or whose insurance coverage is insufficient to cover your damages. It pays for your medical expenses, lost wages, and property damage if the other driver is at fault.

For example, if you are in an accident with a driver who does not have any insurance, your uninsured motorist coverage will pay for your injuries and vehicle repairs up to your policy limits.

Personal Injury Protection (PIP) or Medical Payments Coverage (MedPay)

PIP or MedPay coverage helps pay for your medical expenses, regardless of who is at fault in an accident. This coverage can pay for medical bills, lost wages, and other expenses related to your injuries.

For instance, if you are injured in an accident, PIP or MedPay will cover your medical expenses, even if you are at fault for the accident.

Factors Influencing Insurance Premiums

Your auto insurance premiums are calculated based on a variety of factors. Understanding these factors can help you make informed decisions to potentially lower your premiums.

Factors Influencing Premiums, Auto insurance requirements in my state

Several key factors influence your auto insurance premiums. These factors are assessed by insurance companies to determine your risk level as a driver.

- Age: Younger drivers, particularly those under 25, tend to have higher premiums due to their lack of experience and higher risk of accidents. As you age and gain experience, your premiums may decrease.

- Driving History: Your driving record plays a significant role in determining your premiums. A clean driving history with no accidents or violations will result in lower premiums. Conversely, accidents, speeding tickets, and other violations will increase your premiums.

- Vehicle Type: The type of vehicle you drive impacts your insurance premiums. Sports cars, luxury vehicles, and high-performance cars are often considered higher risk and therefore have higher premiums.

- Location: Your location, including your zip code, influences your premiums. Areas with higher crime rates or more traffic congestion tend to have higher insurance premiums.

- Credit Score: In some states, insurance companies use your credit score to assess your risk. A good credit score can lead to lower premiums, while a poor credit score can result in higher premiums.

- Coverage Levels: The amount of coverage you choose impacts your premiums. Higher coverage levels, such as higher liability limits or comprehensive and collision coverage, will result in higher premiums.

Impact of Driving Violations

Driving violations significantly impact your insurance premiums. The severity of the violation and the frequency of violations influence the increase in your premiums.

- Speeding Tickets: Speeding tickets can increase your premiums by 15% to 30% or more, depending on the severity of the violation and your insurance company’s policies.

- At-Fault Accidents: Accidents where you are found at fault can significantly increase your premiums, sometimes by 50% or more.

- DUI/DWI: Driving under the influence (DUI) or driving while intoxicated (DWI) convictions can result in substantial premium increases, often exceeding 100%.

Premium Differences Based on Varying Factors

The following table illustrates potential premium differences based on various factors. These are just examples and actual premiums may vary based on your specific circumstances and insurance company.

| Factor | Example 1 | Example 2 |

|---|---|---|

| Age | 20-year-old driver | 35-year-old driver |

| Driving History | Clean driving record | One at-fault accident |

| Vehicle Type | Mid-size sedan | Sports car |

| Location | Rural area | Urban area |

| Credit Score | Excellent credit | Poor credit |

| Coverage Levels | Minimum liability coverage | Comprehensive and collision coverage |

| Estimated Premium | $1,000 per year | $2,000 per year |

Obtaining Auto Insurance

Once you understand the auto insurance requirements in your state, the next step is to obtain insurance. This process involves getting quotes, comparing rates, and choosing a policy that meets your needs and budget.

Getting Quotes

Getting quotes is the first step in obtaining auto insurance. You can obtain quotes from multiple insurance companies to compare rates and coverage options. This is crucial for finding the best deal. You can get quotes online, over the phone, or in person.

Comparing Rates

After obtaining quotes, it is important to compare rates carefully. Consider the coverage offered, deductibles, and any discounts available. It’s helpful to use a comparison website to easily compare rates from multiple insurers.

Choosing a Policy

Once you have compared rates, you can choose a policy that best suits your needs and budget. It is essential to read the policy carefully to understand the coverage details, including deductibles, limits, and exclusions.

Selecting an Insurance Provider

Choosing an insurance provider is a crucial decision. Consider the insurer’s financial stability, customer service, and claims handling process. Look for companies with a strong reputation and positive customer reviews.

Negotiating Premium Rates

In some cases, you may be able to negotiate premium rates with your insurer. This may involve discussing your driving history, safety features in your vehicle, and other factors that could influence your rates.

Reviewing Insurance Policies

It is essential to review your insurance policy regularly. Make sure your coverage remains adequate and that you are aware of any changes to the policy terms. You should also review your policy after any major life events, such as getting married, buying a new car, or having a child.

Final Conclusion

Navigating the world of auto insurance can be complex, but by understanding the requirements in your state and choosing the right coverage, you can protect yourself and your finances. Remember, it’s always wise to review your policy regularly and ensure it meets your current needs. By taking proactive steps, you can drive with peace of mind, knowing you’re covered in case of unforeseen events.

Essential FAQs

What happens if I get into an accident without enough insurance?

You could face serious financial consequences, including paying for damages out of pocket, losing your license, and facing legal action.

How often should I review my auto insurance policy?

It’s a good idea to review your policy at least annually, or whenever there’s a significant life change, such as a new car, a change in your driving record, or a move to a new location.

What are some ways to lower my auto insurance premiums?

You can explore options like increasing your deductible, taking a defensive driving course, or bundling your auto insurance with other policies.

Can I get a discount if I have a good driving record?

Yes, many insurance companies offer discounts for drivers with clean driving records. Maintaining a safe driving history can significantly reduce your premiums.