Moving to a new state often means navigating a new set of rules and regulations, and car insurance is no exception. Change car insurance to different state can be a necessary step, ensuring you have the right coverage for your new location and driving needs. State-specific laws and requirements can differ significantly, and driving with outdated insurance can lead to hefty fines or even suspension of your license. This article will guide you through the process of switching your car insurance when you relocate, covering everything from understanding the need for change to finding the right provider for your needs.

Navigating the complexities of changing car insurance can feel overwhelming, but it doesn’t have to be. With a clear understanding of the process and the key factors to consider, you can ensure a smooth transition and maintain adequate coverage throughout your move.

Understanding the Need for Change

Moving to a new state often necessitates a change in your car insurance policy. State laws vary significantly, and what’s considered adequate coverage in one state may not be sufficient in another. This means that simply transferring your existing policy might not be enough to ensure you’re properly protected.

State-Specific Insurance Requirements

Each state has its own set of minimum insurance requirements, known as financial responsibility laws. These laws dictate the minimum amounts of coverage you must have for liability, personal injury protection (PIP), and uninsured/underinsured motorist (UM/UIM) coverage. For example, one state might require a minimum of $25,000 in liability coverage, while another might require $50,000. If you drive with inadequate coverage in a new state, you could face serious consequences, including:

- Fines and penalties: You could be fined for driving without the minimum required coverage.

- License suspension: Your driver’s license could be suspended until you obtain the necessary insurance.

- Legal and financial liability: In case of an accident, you could be held personally liable for damages exceeding your insurance coverage.

Potential Consequences of Outdated Insurance

Driving with outdated insurance in a new state can lead to various problems. These problems can range from financial penalties to legal complications in case of an accident. It’s crucial to ensure your insurance policy meets the requirements of your new state to avoid these potential consequences.

The Process of Changing Insurance

Moving to a new state often involves a change in your car insurance policy. This is due to variations in state laws, insurance regulations, and even driving conditions. Therefore, understanding the process of changing your insurance is crucial for ensuring you have the right coverage and avoid any potential gaps in your protection.

Initiating the Change

The first step in changing your car insurance to a new state is to contact your current insurer. Inform them of your move and the date you plan to relocate. They can help you understand how your current policy will be affected and what options you have.

- Gather Information: Before contacting your insurer, have the following information ready:

- Your policy number

- Your new address

- The date you plan to move

- Details of your vehicle, including make, model, and year

- Discuss Coverage Options: Your current insurer may offer coverage in your new state, but you may need to adjust your policy to meet the specific requirements of your new location. For example, some states require higher liability limits than others.

- Request a Quote: Ask your current insurer for a quote for coverage in your new state. Compare this quote to rates from other insurers in the area to ensure you’re getting the best possible deal.

Obtaining New Coverage

It is essential to secure new insurance coverage before canceling your existing policy. This is to ensure that you are not left without coverage during the transition period.

- Compare Quotes: Get quotes from several insurers in your new state. You can use online comparison websites or contact insurers directly. Be sure to compare coverage options and rates carefully.

- Choose a New Insurer: Once you’ve found a suitable insurer and policy, inform them of your decision. Provide them with all the necessary information, including your new address, vehicle details, and any other relevant information.

- Confirm Effective Date: Ensure that your new policy’s effective date is on or before the date your old policy expires. This will prevent any gaps in coverage.

Canceling Your Existing Policy, Change car insurance to different state

Once your new policy is in effect, you can cancel your existing policy with your previous insurer.

- Provide Notice: Inform your current insurer that you are canceling your policy. They may require you to provide written notice, so it’s best to confirm their requirements.

- Request a Refund: You may be entitled to a refund for any unused portion of your premium. Be sure to inquire about this with your insurer.

- Obtain Confirmation: After canceling your policy, request written confirmation from your insurer that your policy has been canceled. This serves as documentation in case of any future disputes.

Key Factors to Consider

Moving to a new state often involves adjusting your car insurance policy. Insurance rates and coverage options can vary significantly from one state to another, so it’s crucial to understand these differences to ensure you have the right protection at a reasonable price.

Factors Influencing Car Insurance Rates

Several factors contribute to the cost of car insurance in different states. Understanding these factors can help you make informed decisions about your policy.

- Demographics: State demographics, such as population density, age distribution, and income levels, can influence insurance rates. States with higher populations and more drivers often have higher insurance costs due to increased risk of accidents.

- Driving History: Your driving record is a significant factor in determining your insurance premium. States with stricter driving laws or higher accident rates tend to have higher insurance costs for drivers with poor driving records.

- Vehicle Type: The type of vehicle you drive also plays a role in insurance rates. Luxury cars, sports cars, and vehicles with high safety ratings generally have higher insurance premiums.

- Climate: States with severe weather conditions, such as hurricanes, tornadoes, or heavy snowfall, may have higher insurance rates due to the increased risk of damage to vehicles.

- Traffic Congestion: States with heavy traffic congestion may have higher insurance rates due to the increased likelihood of accidents.

- Insurance Regulations: Each state has its own set of insurance regulations, which can affect insurance rates. Some states may have more stringent requirements for coverage, which can lead to higher premiums.

Comparing Coverage Options

The coverage options available in different states can vary, and it’s essential to compare these options to ensure you have the right protection.

- Liability Coverage: This coverage protects you financially if you are at fault in an accident. It covers the other driver’s medical expenses, property damage, and lost wages. The minimum liability coverage required by law varies from state to state.

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if it is damaged in an accident, regardless of who is at fault.

- Comprehensive Coverage: This coverage pays for repairs or replacement of your vehicle if it is damaged due to events other than an accident, such as theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you are involved in an accident with a driver who is uninsured or underinsured. It covers your medical expenses, property damage, and lost wages.

- Personal Injury Protection (PIP): This coverage pays for your medical expenses, lost wages, and other expenses if you are injured in an accident, regardless of who is at fault. It is mandatory in some states.

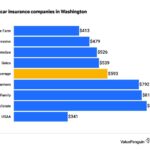

Cost Comparison of Common Coverage Types

The following table provides a general overview of the average annual cost of common insurance coverage types in various states. It’s important to note that these are just estimates, and actual costs may vary depending on individual factors.

| Coverage Type | State 1 | State 2 | State 3 |

|---|---|---|---|

| Liability Coverage (Minimum) | $500 | $600 | $700 |

| Collision Coverage | $400 | $500 | $600 |

| Comprehensive Coverage | $300 | $400 | $500 |

| Uninsured/Underinsured Motorist Coverage | $200 | $300 | $400 |

| Personal Injury Protection (PIP) | $100 | $200 | $300 |

Finding the Right Insurance Provider

Finding the right car insurance provider in a new state is crucial for ensuring you have adequate coverage at a competitive price. The process involves researching and comparing various insurance companies, considering factors like coverage options, pricing, and customer service.

Utilizing Online Comparison Tools

Online comparison tools offer a convenient and efficient way to compare car insurance quotes from multiple providers. These tools gather your basic information, such as your driving history, vehicle details, and location, and then present you with a list of quotes from different insurance companies.

- Popular comparison websites include Insurify, Policygenius, and The Zebra, which allow you to compare quotes from various insurance companies in your new state.

- These tools often offer features like personalized recommendations based on your specific needs and risk profile.

- By using comparison tools, you can save time and effort by avoiding the need to contact each insurance company individually.

Leveraging State-Specific Insurance Directories

Many states maintain online directories that list insurance companies licensed to operate within their boundaries. These directories provide valuable information about each insurer, including their contact details, coverage options, and financial stability ratings.

- For instance, the National Association of Insurance Commissioners (NAIC) website offers a directory of licensed insurance companies by state, which can be a helpful resource for researching providers.

- Additionally, you can check the Department of Insurance website for your new state, as they often provide information on licensed insurers and consumer protection resources.

Obtaining Quotes from Multiple Insurers

Once you have identified potential insurance providers, it’s essential to get quotes from at least three to five companies. This allows you to compare pricing, coverage options, and customer service offerings.

- When requesting quotes, be sure to provide accurate information about your vehicle, driving history, and desired coverage levels.

- It’s also beneficial to ask about any discounts you may qualify for, such as safe driver discounts, good student discounts, or multi-policy discounts.

- Don’t hesitate to negotiate with insurers to try and secure the best possible rates.

Negotiating the Best Rates

Negotiating car insurance rates can be a valuable strategy to lower your premiums. Here are some tips for getting the best possible deal:

- Shop around: Obtain quotes from multiple insurance companies to compare prices and coverage options.

- Bundle your policies: Consider bundling your car insurance with other policies, such as homeowners or renters insurance, to potentially qualify for discounts.

- Improve your driving record: Maintaining a clean driving record can significantly reduce your insurance premiums.

- Increase your deductible: A higher deductible generally results in lower premiums, but be sure to choose a deductible you can comfortably afford in case of an accident.

- Ask about discounts: Inquire about any available discounts, such as safe driver discounts, good student discounts, or multi-policy discounts.

Additional Considerations: Change Car Insurance To Different State

While switching car insurance can be a smooth process, there are potential challenges you might encounter. It’s crucial to be aware of these challenges and take necessary steps to mitigate them.

Transferring Existing Claims

When changing insurance providers, it’s important to understand how your existing claims will be handled. You may need to provide your new insurer with documentation of your previous claims, including details about the incident, the claim amount, and the settlement process. This information helps your new insurer assess your risk profile and determine your premium.

Dealing with Insurance Disputes

Disputes can arise when switching insurance providers, especially if there are outstanding claims or unresolved issues with your previous insurer. If you encounter a dispute, it’s important to document all communication with both insurers and keep accurate records of all correspondence, including emails, letters, and phone calls. You may also want to consider seeking assistance from a consumer protection agency or a legal professional.

Keeping Accurate Records

Maintaining accurate records of your insurance policies is crucial, regardless of whether you’re switching providers or not. This includes keeping copies of your policy documents, communication with your insurers, and any claim-related documentation. These records can be helpful if you need to file a claim or resolve a dispute with your insurer.

Relevant Resources

There are various resources available to help you navigate the process of changing car insurance and address any potential challenges. Here are some helpful resources:

- State Insurance Departments: Each state has an insurance department that regulates insurance companies and provides consumer protection. You can contact your state insurance department to file a complaint, get information about insurance companies, or seek guidance on your insurance rights.

- Consumer Protection Agencies: Consumer protection agencies, such as the Better Business Bureau (BBB) and the National Association of Insurance Commissioners (NAIC), can provide information about insurance companies and help you resolve disputes with insurers.

- Insurance Industry Associations: Insurance industry associations, such as the American Insurance Association (AIA) and the Independent Insurance Agents & Brokers of America (IIABA), provide resources and information about the insurance industry.

Last Recap

Moving to a new state requires adapting to new environments and regulations, and car insurance is no exception. By understanding the need for change, carefully following the steps involved, and considering key factors like coverage options and rates, you can navigate this transition seamlessly. Remember to research different providers, compare quotes, and choose the policy that best suits your individual needs and driving habits. With a little planning and preparation, changing your car insurance when moving states can be a straightforward process, ensuring you’re protected on the road in your new home.

Questions and Answers

What happens if I don’t change my car insurance when I move?

Driving with outdated insurance in a new state can result in fines, license suspension, and even denial of coverage in the event of an accident.

How long do I have to change my insurance after moving?

Most states require you to update your insurance within 30 days of moving. It’s best to contact your insurer as soon as possible to avoid any delays or potential issues.

Can I keep my current insurance provider when I move?

While some insurers offer coverage in multiple states, it’s best to check with your current provider to confirm their coverage area. You may need to switch to a new insurer if your current one doesn’t operate in your new state.