Homeowners insurance new york state – Homeowners insurance in New York State is essential for protecting your most valuable asset – your home. This comprehensive guide delves into the intricacies of this crucial insurance, providing insights into coverage options, premiums, and navigating the claims process. From understanding the mandatory requirements to navigating the insurance market, we’ll explore the key aspects of securing the right homeowners insurance for your needs.

New York, with its diverse landscapes and potential risks, presents unique challenges for homeowners. This guide will equip you with the knowledge to make informed decisions about your insurance coverage, ensuring peace of mind and financial security.

Understanding Homeowners Insurance in New York State

Homeowners insurance is a crucial component of protecting your most valuable asset – your home. In New York State, where weather events like hurricanes and blizzards are common, having adequate insurance coverage is essential. Homeowners insurance provides financial protection against various risks that could jeopardize your home and belongings.

Coverage Included in a Standard Policy

A standard homeowners insurance policy in New York offers comprehensive coverage, safeguarding your home and possessions against a wide range of potential perils. Here’s a detailed breakdown of the different types of coverage included:

- Dwelling Coverage: This covers the physical structure of your home, including the attached structures like garages and decks. It protects against damage from events like fire, windstorms, hail, vandalism, and more.

- Other Structures Coverage: This covers detached structures on your property, such as sheds, fences, and swimming pools, against similar perils as dwelling coverage.

- Personal Property Coverage: This protects your belongings inside your home, such as furniture, appliances, electronics, clothing, and jewelry, against covered perils.

- Liability Coverage: This provides financial protection if you are held liable for injuries or property damage to others on your property.

- Medical Payments Coverage: This covers medical expenses for guests who are injured on your property, regardless of who is at fault.

- Loss of Use Coverage: This provides financial assistance if you are unable to live in your home due to a covered loss, covering expenses like temporary housing and living costs.

Factors Influencing Homeowners Insurance Premiums

Several factors determine the cost of your homeowners insurance premiums in New York. These factors include:

Baca Juga

- Location: The risk of natural disasters, crime rates, and other factors specific to your location can significantly impact your premiums. Homes in areas prone to hurricanes, floods, or earthquakes may face higher premiums.

- Property Value: The higher the value of your home, the more expensive it is to rebuild or repair, leading to higher premiums.

- Coverage Levels: The amount of coverage you choose for your home and belongings directly affects your premium. Higher coverage levels generally result in higher premiums.

- Deductible: Your deductible is the amount you agree to pay out-of-pocket for covered losses before your insurance kicks in. A higher deductible generally leads to lower premiums.

- Home Features: Features like security systems, fire alarms, and sprinkler systems can reduce your premium by lowering the risk of claims.

- Claims History: Past claims on your insurance can impact your future premiums. A history of frequent claims may result in higher premiums.

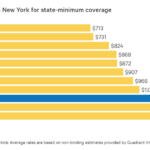

New York State’s Unique Insurance Requirements: Homeowners Insurance New York State

New York State has specific insurance requirements for homeowners, ensuring adequate coverage for potential losses. These requirements vary depending on the type of property and its location. Understanding these regulations is crucial for homeowners to protect themselves financially.

Coverage Requirements for Different Property Types

New York State mandates specific coverage levels for different types of properties. This ensures that homeowners have adequate protection for their investments.

- Single-family homes: These homes are typically required to have a minimum of $1 million in liability coverage and $50,000 in personal property coverage. This coverage is essential for protecting homeowners from financial losses due to accidents or injuries that occur on their property.

- Condominiums: Condo owners in New York State are typically required to purchase a condo unit-owners policy. This policy provides coverage for the interior of the unit and personal property. It also includes liability coverage for accidents that occur within the unit.

- Multi-family dwellings: Owners of multi-family dwellings must carry insurance that covers the entire building, including common areas and individual units. The coverage requirements are typically higher than for single-family homes, reflecting the increased risk associated with multiple tenants.

State-Specific Regulations and Laws

New York State has several regulations and laws that impact homeowners insurance policies. These regulations aim to protect both homeowners and insurance companies.

- New York State’s Fair Plan: This plan provides insurance to homeowners who have difficulty obtaining coverage in the private market due to factors like high risk or location. The Fair Plan offers basic coverage, ensuring that all homeowners have access to insurance.

- Flood Insurance: In areas prone to flooding, homeowners may be required to purchase flood insurance. This coverage is separate from standard homeowners insurance and protects against losses caused by flooding.

- Earthquake Coverage: While not mandatory, homeowners in areas with a high risk of earthquakes may consider purchasing earthquake insurance. This coverage protects against damage caused by earthquakes, which is typically excluded from standard homeowners policies.

Navigating the Insurance Market in New York

Choosing the right homeowners insurance policy in New York can feel overwhelming with so many insurance companies vying for your business. It’s crucial to compare different providers and their offerings to find the best fit for your needs and budget.

Comparing Insurance Providers in New York

Understanding the key differences between insurance companies in New York can help you make an informed decision. Here’s a comparison of some of the most prominent providers, highlighting their coverage options, customer service, and pricing structures:

| Provider | Coverage Options | Customer Service | Pricing |

|---|---|---|---|

| Liberty Mutual | Offers a wide range of coverage options, including personal liability, dwelling coverage, and personal property coverage. They also provide optional endorsements for specific risks, such as flood insurance. | Known for their responsive customer service and easy-to-use online platform. | Pricing varies based on factors like your home’s location, value, and coverage options. |

| State Farm | Offers comprehensive homeowners insurance policies with various coverage options, including personal liability, dwelling coverage, and personal property coverage. | Highly rated for their customer service and claims handling process. | Known for their competitive pricing and discounts for bundling policies. |

| Allstate | Provides a wide range of homeowners insurance policies with various coverage options, including personal liability, dwelling coverage, and personal property coverage. | Offers online and phone support, as well as local agents for personalized assistance. | Pricing is competitive, with various discounts available for safety features and bundling policies. |

| Chubb | Specializes in high-value homes and offers comprehensive coverage options, including personal liability, dwelling coverage, and personal property coverage. | Known for their exceptional customer service and personalized attention to high-net-worth clients. | Pricing reflects their high-end services and comprehensive coverage options. |

Obtaining Homeowners Insurance Quotes

Getting homeowners insurance quotes from multiple providers is essential to finding the best value for your money. Here’s a step-by-step guide to obtaining quotes:

- Gather your information: This includes your address, property details, coverage needs, and any relevant claims history.

- Contact multiple insurance providers: You can request quotes online, over the phone, or through local agents.

- Compare quotes: Carefully review each quote, considering coverage options, deductibles, premiums, and customer service ratings.

- Choose the best policy: Select the policy that offers the best value for your needs and budget, balancing coverage options with affordability.

Selecting the Right Policy

When choosing a homeowners insurance policy, it’s crucial to consider factors like:

- Coverage options: Ensure the policy covers your home’s structure, personal property, and liability risks.

- Deductibles: A higher deductible typically leads to lower premiums, but you’ll pay more out-of-pocket in case of a claim.

- Premiums: Compare premiums from different providers and consider factors like discounts and bundling options.

- Customer service: Look for providers with a good reputation for customer service and claims handling.

- Financial stability: Choose a provider with a strong financial rating to ensure they can pay out claims if needed.

Common Homeowner Risks in New York

Living in New York State comes with its own set of challenges, especially for homeowners. From unpredictable weather to potential property damage, navigating these risks is crucial for safeguarding your home and finances.

Natural Disasters

Natural disasters pose a significant threat to homeowners in New York. The state experiences a variety of weather events, including hurricanes, blizzards, floods, and tornadoes, each carrying its own unique risks.

Potential Consequences and Coverage

| Risk | Potential Consequences | Homeowners Insurance Coverage |

|---|---|---|

| Hurricanes | Wind damage, flooding, power outages, and structural damage | Wind damage is typically covered, but flood damage requires separate flood insurance. |

| Blizzards | Snow accumulation, roof collapse, power outages, and frozen pipes | Coverage for snow damage, but frozen pipes may require specific endorsements. |

| Floods | Water damage to the structure, belongings, and foundation | Flood insurance is a separate policy and not typically included in homeowners insurance. |

| Tornadoes | Wind damage, flying debris, and structural damage | Wind damage is generally covered, but damage caused by flying debris may have limitations. |

Mitigating Risks

- Hurricane preparedness: Secure loose objects, trim trees, and have an emergency plan in place.

- Winterizing your home: Insulate pipes, clear gutters, and have a backup heating source.

- Flood mitigation: Elevate belongings, install sump pumps, and consider flood insurance.

- Tornado awareness: Stay informed about weather forecasts and have a designated safe room.

Theft

Theft is a significant concern for homeowners in New York, especially in urban areas. Burglary, larceny, and vandalism can lead to property damage, loss of belongings, and emotional distress.

Potential Consequences and Coverage

| Risk | Potential Consequences | Homeowners Insurance Coverage |

|---|---|---|

| Burglary | Loss of belongings, damage to property, and emotional distress | Coverage for stolen belongings and damage to the property, subject to policy limits. |

| Larceny | Theft of belongings from the property or surrounding areas | Coverage for stolen belongings, but may have limitations depending on the type of larceny. |

| Vandalism | Damage to property, including graffiti, broken windows, and destruction of belongings | Coverage for vandalism damage, but may have deductibles and limits. |

Mitigating Risks

- Home security: Install alarm systems, security cameras, and motion sensor lights.

- Secure belongings: Keep valuable items in a safe or locked storage area.

- Be vigilant: Report suspicious activity to the police and be aware of your surroundings.

- Neighborhood watch: Participate in neighborhood watch programs to deter crime.

Liability Claims

Homeowners are responsible for injuries or damages that occur on their property. Liability claims can arise from accidents, negligence, or even the actions of guests.

Potential Consequences and Coverage

| Risk | Potential Consequences | Homeowners Insurance Coverage |

|---|---|---|

| Slip and fall accidents | Injuries to visitors, legal expenses, and medical costs | Coverage for legal expenses and medical costs, subject to policy limits. |

| Dog bites | Injuries to individuals, legal expenses, and medical costs | Coverage for legal expenses and medical costs, but may have breed restrictions. |

| Negligence | Damage to a neighbor’s property, injuries to individuals, and legal expenses | Coverage for legal expenses and damage to property, subject to policy limits. |

Mitigating Risks

- Maintain a safe property: Repair hazards, clear walkways, and ensure adequate lighting.

- Train pets: Properly train dogs and keep them on a leash when necessary.

- Guest awareness: Be mindful of guest behavior and ensure they are aware of potential risks.

- Liability waivers: Consider using liability waivers for certain activities or events.

Understanding Coverage Options and Exclusions

A homeowner’s insurance policy in New York State offers comprehensive protection for your property and personal belongings. It’s crucial to understand the different coverage options and exclusions within the policy to ensure you’re adequately protected.

Coverage Options

Homeowner’s insurance policies in New York provide various coverage options designed to protect your property and financial interests. These options typically include:

- Dwelling Coverage: This coverage protects the physical structure of your home, including the attached structures like garages and decks, against covered perils. It helps pay for repairs or replacement costs if your home is damaged by fire, windstorms, vandalism, or other covered events.

- Personal Property Coverage: This coverage protects your belongings inside your home, such as furniture, appliances, clothing, and electronics. It helps cover the cost of replacement or repair if these items are damaged or stolen.

- Liability Coverage: This coverage protects you from financial losses if someone is injured on your property or if you cause damage to someone else’s property. For example, if a guest trips and falls on your icy driveway, liability coverage helps pay for their medical expenses and legal costs.

- Additional Living Expenses: This coverage helps pay for temporary housing and other essential living expenses if you are unable to live in your home due to a covered event. For instance, if your home is damaged by a fire, this coverage helps pay for hotel costs, meals, and other necessities while your home is being repaired.

Common Exclusions

While homeowner’s insurance offers extensive coverage, there are certain situations where coverage may be limited or excluded. These exclusions are typically Artikeld in the policy and may include:

- Acts of War: Coverage typically excludes damage caused by acts of war, such as bombing or military action.

- Intentional Damage: Insurance policies generally do not cover damage caused intentionally by the policyholder or someone acting on their behalf. This includes situations like arson or deliberate vandalism.

- Certain Types of Business Activities: Homeowner’s insurance policies typically exclude coverage for business activities conducted from your home. For example, if you run a small business from your home and it is damaged, the policy may not cover the business-related losses.

Situations with Limited or Excluded Coverage

It’s important to understand specific situations where coverage may be limited or excluded under a standard homeowner’s insurance policy. Some examples include:

- Earthquakes: Most standard homeowner’s insurance policies in New York do not cover earthquake damage. You may need to purchase separate earthquake insurance to protect your home from this specific peril.

- Flooding: Standard homeowner’s insurance policies typically do not cover flood damage. If you live in a flood-prone area, you need to purchase flood insurance separately through the National Flood Insurance Program (NFIP).

- Mold Damage: Coverage for mold damage is often limited or excluded under standard policies. The policy may only cover mold damage caused by a covered event, such as a water leak. If the mold is caused by poor maintenance or other factors not covered by the policy, you may be responsible for the repair costs.

Filing a Claim and Navigating the Claims Process

Experiencing property damage or loss can be stressful, and filing a homeowners insurance claim in New York State can seem overwhelming. However, understanding the process and knowing your rights can make navigating this challenging situation smoother. This section will guide you through the steps involved in filing a claim, provide tips for documenting damages, and address common challenges you might encounter.

Steps Involved in Filing a Claim

The first step is to contact your insurance company as soon as possible after the incident. This could be a storm, fire, theft, or any other event covered by your policy. Your insurance provider will provide you with instructions on how to file a claim and will assign a claims adjuster to your case.

- Contact your insurance company immediately: Inform them about the incident and the extent of the damage. This allows them to initiate the claims process and guide you through the necessary steps.

- File a claim: Your insurance company will provide you with a claim form or an online portal to file your claim. Be sure to provide all the necessary information, including details about the incident, the date and time of the event, and a list of damaged property.

- Cooperate with the claims adjuster: The claims adjuster will investigate the incident and assess the damages. Be prepared to provide them with access to your property, documentation, and any relevant information.

- Review the claim settlement: Once the claims adjuster completes their investigation, they will provide you with a settlement offer. Carefully review the offer and ensure it covers all the damages and expenses you are entitled to. If you disagree with the offer, you have the right to negotiate or file an appeal.

Documenting Damages and Gathering Information

Thorough documentation is crucial for a successful claim. It helps you and your insurance company accurately assess the damages and ensure you receive the appropriate compensation.

- Take photos and videos: Capture images of the damaged property from multiple angles, focusing on the extent of the damage. Videos can be particularly helpful for demonstrating the impact of the incident.

- Keep receipts and invoices: Save all receipts and invoices related to repairs or replacements. This documentation helps you demonstrate the actual cost of the damages.

- Make a detailed list of damaged items: Include the name, brand, model, and purchase date for each item. This list will help you estimate the value of the damaged property.

- Create a timeline of events: Document the date and time of the incident, the steps you took to mitigate the damage, and any communication with your insurance company.

Common Challenges and Guidance

The claims process can be complex, and homeowners often encounter challenges. Understanding these challenges and how to navigate them can make the process smoother.

- Delayed responses from the insurance company: It’s common for insurance companies to take some time to process claims, especially if the damages are extensive. Be patient and keep track of your communication with the insurance company. If you feel your claim is being delayed unreasonably, reach out to your insurance agent or file a complaint with the New York State Department of Financial Services.

- Disputes over the settlement offer: You may disagree with the insurance company’s assessment of the damages or the amount they offer to settle your claim. If this happens, be prepared to negotiate or file an appeal. It’s helpful to have supporting documentation, such as estimates from contractors or receipts for repairs, to support your position.

- Dealing with contractors: The claims process may involve working with contractors to repair or replace damaged property. Be sure to choose reputable contractors and get multiple estimates before making any decisions.

Additional Considerations for New York Homeowners

New York State presents unique challenges and considerations for homeowners, beyond the standard requirements of homeowners insurance. It’s crucial to understand these additional factors to ensure comprehensive coverage and financial protection.

Flood Insurance, Homeowners insurance new york state

Flood insurance is essential for homeowners residing in flood-prone areas of New York State. The National Flood Insurance Program (NFIP) provides flood insurance policies, which are often required by mortgage lenders for properties located in designated flood zones.

- Flood zones are areas identified by the Federal Emergency Management Agency (FEMA) as having a significant risk of flooding.

- Flood insurance policies cover damages caused by flooding, including water damage, structural damage, and personal property loss.

- Standard homeowners insurance policies typically do not cover flood damage. Therefore, homeowners in flood-prone areas must obtain separate flood insurance.

Earthquake Insurance

While New York State is not known for frequent earthquakes, some regions, particularly in the western part of the state, are susceptible to seismic activity. For homeowners in these areas, earthquake insurance is an important consideration.

- Earthquake insurance provides coverage for damages caused by earthquakes, including structural damage, foundation damage, and personal property loss.

- Standard homeowners insurance policies typically do not cover earthquake damage. Therefore, homeowners in earthquake-prone areas should consider obtaining earthquake insurance.

Umbrella Insurance

Umbrella insurance provides additional liability coverage beyond the limits of your standard homeowners insurance policy. This type of insurance can be particularly beneficial for homeowners who:

- Have significant assets, such as investments, savings, or valuable possessions.

- Engage in activities that carry a higher risk of liability, such as hosting large gatherings or owning a swimming pool.

- Are concerned about potential lawsuits, even if they are not at fault.

Closing Summary

Navigating the complexities of homeowners insurance in New York State can seem daunting, but with the right information and understanding, it can be a straightforward process. By understanding your coverage options, evaluating risks, and choosing the right insurance provider, you can safeguard your home and your future. Remember to review your policy regularly, ensuring it aligns with your changing needs and providing you with the peace of mind you deserve.

FAQ Summary

What are the main types of coverage included in a homeowners insurance policy in New York State?

Homeowners insurance in New York typically includes dwelling coverage (protecting the structure of your home), personal property coverage (covering belongings inside your home), liability coverage (protecting you from lawsuits), and additional living expenses (covering temporary housing if your home is uninhabitable).

How do I choose the right homeowners insurance provider in New York?

It’s essential to compare quotes from multiple insurance companies, considering factors like coverage options, customer service, and pricing. Look for companies with a good reputation, strong financial stability, and a history of fair claims handling.

What are some common exclusions in homeowners insurance policies in New York?

Common exclusions include damage caused by acts of war, intentional damage, and certain types of business activities. It’s crucial to carefully review your policy to understand the specific exclusions that apply.

How do I file a claim with my homeowners insurance provider in New York?

Contact your insurance provider immediately after an incident. Document the damage with photos and videos, and gather any relevant information, such as police reports or witness statements. Follow the provider’s instructions for filing the claim.