Auto insurance minimums by state are a crucial aspect of responsible driving, ensuring financial protection in the event of an accident. These minimums, mandated by each state, represent the least amount of coverage required to legally operate a vehicle. Understanding these requirements is essential for drivers, as failing to meet them can lead to significant financial and legal repercussions.

State laws dictate the minimum coverage levels for bodily injury liability, property damage liability, uninsured/underinsured motorist coverage, and personal injury protection (PIP). These coverage types offer protection against various risks, such as injuries to others, damage to property, and medical expenses. However, minimums can vary widely depending on the state, reflecting factors like population density, accident rates, and economic conditions.

Introduction to Auto Insurance Minimums: Auto Insurance Minimums By State

Auto insurance is a crucial financial safety net that protects you and your finances in case of an accident or other unforeseen events involving your vehicle. It helps cover costs associated with property damage, injuries, and legal liabilities arising from such incidents. However, not all auto insurance policies are created equal. Each state in the United States mandates minimum coverage levels that drivers must carry, known as minimum insurance requirements. These requirements vary significantly from state to state, and understanding them is essential for ensuring you are adequately protected and compliant with the law.

Why States Mandate Minimum Coverage Levels

States mandate minimum coverage levels to protect drivers, passengers, and pedestrians from the financial consequences of accidents. By requiring drivers to carry at least a certain level of insurance, states aim to ensure that victims of accidents have access to compensation for their injuries, medical expenses, and property damage. These minimum coverage levels act as a safety net for both the insured and the uninsured, ensuring that financial burdens do not fall solely on the victims of accidents.

State-Specific Minimum Requirements

Every state in the United States has its own set of minimum auto insurance requirements that drivers must meet to legally operate a vehicle. These requirements vary significantly from state to state, and understanding them is crucial for ensuring you have adequate coverage in case of an accident.

State-Specific Minimum Coverage Requirements

To illustrate the wide range of minimum coverage requirements, here’s a table summarizing the minimums for each state:

| State | Bodily Injury Liability (per person/per accident) | Property Damage Liability | Uninsured/Underinsured Motorist Coverage | Personal Injury Protection (PIP) |

|---|---|---|---|---|

| Alabama | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Alaska | $50,000/$100,000 | $25,000 | $50,000/$100,000 | Optional |

| Arizona | $25,000/$50,000 | $15,000 | $25,000/$50,000 | Optional |

| Arkansas | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| California | $15,000/$30,000 | $5,000 | $15,000/$30,000 | Optional |

| Colorado | $25,000/$50,000 | $15,000 | $25,000/$50,000 | Optional |

| Connecticut | $20,000/$40,000 | $10,000 | $20,000/$40,000 | Mandatory |

| Delaware | $30,000/$60,000 | $10,000 | $30,000/$60,000 | Optional |

| Florida | $10,000/$20,000 | $10,000 | $10,000/$20,000 | Mandatory |

| Georgia | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Hawaii | $20,000/$40,000 | $10,000 | $20,000/$40,000 | Optional |

| Idaho | $25,000/$50,000 | $15,000 | $25,000/$50,000 | Optional |

| Illinois | $20,000/$40,000 | $15,000 | $20,000/$40,000 | Optional |

| Indiana | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Iowa | $20,000/$40,000 | $15,000 | $20,000/$40,000 | Optional |

| Kansas | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Kentucky | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Louisiana | $15,000/$30,000 | $10,000 | $15,000/$30,000 | Mandatory |

| Maine | $50,000/$100,000 | $25,000 | $50,000/$100,000 | Optional |

| Maryland | $30,000/$60,000 | $15,000 | $30,000/$60,000 | Optional |

| Massachusetts | $20,000/$40,000 | $5,000 | $20,000/$40,000 | Mandatory |

| Michigan | $20,000/$40,000 | $10,000 | $20,000/$40,000 | Mandatory |

| Minnesota | $30,000/$60,000 | $10,000 | $30,000/$60,000 | Mandatory |

| Mississippi | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Missouri | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Montana | $25,000/$50,000 | $20,000 | $25,000/$50,000 | Optional |

| Nebraska | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Nevada | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| New Hampshire | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| New Jersey | $15,000/$30,000 | $5,000 | $15,000/$30,000 | Mandatory |

| New Mexico | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| New York | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Mandatory |

| North Carolina | $30,000/$60,000 | $25,000 | $30,000/$60,000 | Optional |

| North Dakota | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Ohio | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Oklahoma | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Oregon | $25,000/$50,000 | $20,000 | $25,000/$50,000 | Optional |

| Pennsylvania | $15,000/$30,000 | $5,000 | $15,000/$30,000 | Optional |

| Rhode Island | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Mandatory |

| South Carolina | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| South Dakota | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

| Tennessee | $25,000/$50,000 | $15,000 | $25,000/$50,000 | Optional |

| Texas | $30,000/$60,000 | $25,000 | $30,000/$60,000 | Optional |

| Utah | $25,000/$65,000 | $15,000 | $25,000/$65,000 | Optional |

| Vermont | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Virginia | $25,000/$50,000 | $20,000 | $25,000/$50,000 | Optional |

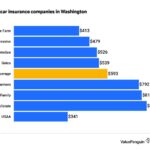

| Washington | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| West Virginia | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Optional |

| Wisconsin | $25,000/$50,000 | $10,000 | $25,000/$50,000 | Mandatory |

| Wyoming | $25,000/$50,000 | $25,000 | $25,000/$50,000 | Optional |

This table highlights the differences in minimum coverage requirements across states. Let’s delve deeper into each coverage type and its implications:

* Bodily Injury Liability: This coverage protects you financially if you cause an accident that injures another person. It covers their medical expenses, lost wages, and pain and suffering. The limits indicate the maximum amount your insurance will pay per person and per accident. For example, if you have $25,000/$50,000 bodily injury liability coverage, your insurance will pay up to $25,000 for injuries to any one person and up to $50,000 for all injuries in a single accident.

* Property Damage Liability: This coverage protects you financially if you cause an accident that damages another person’s property. It covers the cost of repairs or replacement of the damaged property. The limit indicates the maximum amount your insurance will pay for property damage in a single accident.

* Uninsured/Underinsured Motorist Coverage: This coverage protects you if you are involved in an accident with an uninsured or underinsured driver. It covers your medical expenses, lost wages, and pain and suffering. The limits indicate the maximum amount your insurance will pay per person and per accident.

* Personal Injury Protection (PIP): This coverage, often called “no-fault” coverage, pays for your medical expenses and lost wages regardless of who caused the accident. It is mandatory in some states, but optional in others.

These coverage types and their limits vary significantly depending on the state. For example, Florida has a low bodily injury liability minimum of $10,000/$20,000, while Maine has a much higher minimum of $50,000/$100,000. Similarly, some states, like Connecticut and Massachusetts, require PIP coverage, while others, like Alabama and Alaska, do not.

Factors Influencing Minimum Coverage

States carefully consider several factors when establishing minimum auto insurance coverage requirements. These factors aim to strike a balance between protecting drivers and ensuring affordability for policyholders.

Impact of Population Density

Population density plays a significant role in determining minimum coverage levels. States with high population density, like New York City or Los Angeles, often have stricter minimum coverage requirements. This is because a higher concentration of vehicles increases the likelihood of accidents and potential for significant damages. Consequently, higher minimum coverage levels help ensure adequate financial protection for victims in the event of an accident.

Influence of Accident Rates

States with higher accident rates tend to have more stringent minimum coverage requirements. This is because a higher frequency of accidents translates to a greater need for financial protection for victims. By increasing minimum coverage levels, states aim to ensure that injured parties receive sufficient compensation for their medical expenses, lost wages, and property damage.

Economic Conditions

Economic conditions also influence minimum coverage requirements. States with a strong economy may have higher minimum coverage levels, reflecting the higher value of vehicles and the potential for greater financial losses in accidents. Conversely, states experiencing economic hardship may have lower minimum coverage requirements to make insurance more affordable for residents.

State-Specific Laws and Regulations

State-specific laws and regulations play a crucial role in shaping minimum coverage requirements. For instance, some states mandate specific coverage types, such as uninsured motorist coverage, which protects drivers from financial losses caused by uninsured or underinsured motorists. These laws and regulations ensure that all drivers have adequate protection, regardless of the financial responsibility of other parties involved in an accident.

Understanding Coverage Types

Understanding the different types of auto insurance coverage is crucial for making informed decisions about your policy. Auto insurance policies offer various coverage options, each designed to protect you and your vehicle in specific situations. These coverages are designed to address different types of risks associated with driving.

Bodily Injury Liability Coverage

This coverage protects you financially if you cause an accident that injures another person. It covers the medical expenses, lost wages, and other damages the injured party may incur due to the accident.

Bodily injury liability coverage is typically expressed as a per-person limit and a per-accident limit. For example, 25/50 coverage means your insurance will pay up to $25,000 per person injured and up to $50,000 for all injuries in a single accident.

Property Damage Liability Coverage

This coverage protects you financially if you cause an accident that damages another person’s property, such as their vehicle or other belongings. It covers the cost of repairs or replacement of the damaged property.

Property damage liability coverage is usually expressed as a single limit, such as $50,000. This means your insurance will pay up to $50,000 for all property damage caused in a single accident.

Uninsured/Underinsured Motorist Coverage

This coverage protects you financially if you are involved in an accident with a driver who is uninsured or underinsured. It covers your medical expenses, lost wages, and other damages if the other driver’s insurance is insufficient to cover your losses.

Uninsured/underinsured motorist coverage is typically expressed as a per-person limit and a per-accident limit, similar to bodily injury liability coverage.

Personal Injury Protection (PIP)

This coverage, also known as no-fault insurance, covers your medical expenses, lost wages, and other damages, regardless of who caused the accident. It applies even if you are at fault for the accident.

PIP coverage is typically expressed as a per-person limit, such as $10,000.

Visual Representation of Coverage Types

Visual Representation: Imagine a circle divided into four quadrants.

* Quadrant 1: Bodily Injury Liability Coverage – This quadrant represents your responsibility to others for injuries caused by your vehicle.

* Quadrant 2: Property Damage Liability Coverage – This quadrant represents your responsibility to others for property damage caused by your vehicle.

* Quadrant 3: Uninsured/Underinsured Motorist Coverage – This quadrant represents protection against drivers who lack or have insufficient insurance.

* Quadrant 4: Personal Injury Protection (PIP) – This quadrant represents your protection, regardless of fault, for injuries and expenses resulting from an accident.

This visual representation highlights the scope of each coverage type and their respective roles in protecting you and your finances in the event of an accident.

Consequences of Insufficient Coverage

Driving without adequate auto insurance coverage can have serious financial and legal repercussions, potentially leading to significant debt, legal battles, and even the loss of your driver’s license. Understanding the potential consequences is crucial to making informed decisions about your insurance needs.

Financial Risks

Insufficient coverage can lead to significant financial burdens. In the event of an accident, you may be responsible for covering costs that exceed your insurance policy limits. These costs can include:

- Medical expenses: If you cause an accident resulting in injuries to others, you may be held liable for their medical bills, even if you were not at fault.

- Property damage: You could be responsible for repairing or replacing damaged vehicles or property belonging to others.

- Lost wages: If you are unable to work due to injuries sustained in an accident, you may have to cover your own lost wages.

- Legal fees: You may need to hire an attorney to represent you in court, which can be expensive.

Legal Liabilities, Auto insurance minimums by state

Driving without sufficient insurance coverage can result in legal consequences. Depending on the severity of the accident and the state laws, you may face:

- Fines and penalties: Driving without the minimum required insurance coverage is often considered a violation of state law and can result in fines and penalties.

- License suspension: In some cases, your driver’s license may be suspended or revoked if you are found to be driving without sufficient insurance coverage.

- Jail time: In extreme cases, driving without insurance can even lead to jail time, especially if the accident resulted in serious injuries or death.

Real-Life Scenarios

Here are some real-life scenarios that illustrate the importance of adequate auto insurance coverage:

- Scenario 1: A driver with minimum liability coverage causes an accident that results in significant injuries to another driver. The injured driver’s medical bills exceed the driver’s liability coverage limits. The at-fault driver is then held responsible for the remaining medical costs, potentially leading to substantial debt and financial hardship.

- Scenario 2: A driver with insufficient collision coverage is involved in an accident that damages their vehicle. The cost of repairs exceeds their collision coverage limit, leaving the driver responsible for the remaining costs.

- Scenario 3: A driver without uninsured motorist coverage is hit by an uninsured driver. The uninsured driver is unable to pay for the damages, leaving the injured driver to bear the costs.

Tips for Choosing the Right Coverage

Determining the right level of auto insurance coverage is crucial for protecting yourself financially in case of an accident. It involves a careful assessment of your individual needs and circumstances, considering factors like your driving habits, the value of your vehicle, and your personal financial situation.

Factors to Consider

It’s important to consider several factors when deciding on the right auto insurance coverage. This will help you determine the appropriate level of protection for your specific needs.

- Driving Habits: Drivers with a clean record and low mileage typically require less coverage than those with frequent accidents or high mileage. For instance, a driver with a history of speeding tickets or accidents may need higher liability limits to protect themselves from potential lawsuits.

- Vehicle Value: The value of your vehicle is a significant factor in determining the amount of collision and comprehensive coverage you need. If your vehicle is new or high-value, you may need more coverage to ensure you receive adequate compensation in case of damage or theft.

- Personal Financial Situation: Your financial situation also plays a role. If you have limited assets, you may want to consider higher liability limits to protect yourself from potential financial ruin in case of a serious accident.

Comparing Quotes and Selecting the Best Policy

Once you’ve considered these factors, it’s time to compare quotes from different insurance companies. This will help you find the best policy that meets your needs and budget.

- Shop Around: Obtain quotes from multiple insurance companies. You can use online comparison websites or contact insurance agents directly. This will give you a good idea of the available options and pricing.

- Consider Deductibles: A higher deductible typically means a lower premium, but you’ll pay more out of pocket if you file a claim. Choose a deductible that you can comfortably afford in case of an accident.

- Review Coverage Options: Carefully review the coverage options offered by each insurer. Ensure that the policy includes the minimum required coverage for your state, as well as any additional coverage you deem necessary. For example, you may want to consider uninsured/underinsured motorist coverage for added protection in case of an accident with a driver who doesn’t have adequate insurance.

- Read the Fine Print: Before making a decision, thoroughly read the policy documents. Pay attention to exclusions, limitations, and any specific conditions that may affect your coverage.

Resources for Further Information

While this guide provides a comprehensive overview of auto insurance minimums, you may need further information specific to your situation. Thankfully, numerous resources can help you gather more details and make informed decisions about your auto insurance coverage.

Official State Government Websites

Each state has its own Department of Insurance or a similar agency responsible for regulating the insurance industry. These websites offer valuable information on state-specific minimum insurance requirements, consumer protection tips, and resources for filing complaints.

- For example, you can visit the California Department of Insurance website for information about auto insurance requirements in California.

- Similarly, the New York State Department of Financial Services website provides information on auto insurance requirements in New York.

Insurance Companies

Directly contacting insurance companies can provide you with specific quotes, coverage options, and details about their policies. Many insurance companies have comprehensive websites with information about their products, services, and customer support resources.

- For example, GEICO and Progressive are popular insurance companies that offer online tools and resources for comparing quotes and understanding coverage options.

Consumer Protection Organizations

Consumer protection organizations play a crucial role in advocating for consumers’ rights and providing information about various financial products and services. These organizations often offer unbiased advice, complaint resolution services, and educational resources on auto insurance.

- The Insurance Information Institute provides information on various insurance topics, including auto insurance, and offers resources for consumers.

- The National Association of Insurance Commissioners is a non-profit organization that represents state insurance regulators and provides information on insurance regulations and consumer protection.

Insurance Agents or Brokers

For personalized advice and assistance with choosing the right auto insurance coverage, consider consulting with a licensed insurance agent or broker. They can help you understand your specific needs, compare different policies, and find the best coverage at a competitive price.

Ending Remarks

Navigating the complex world of auto insurance can be daunting, but understanding state minimums is a crucial first step. By familiarizing yourself with the requirements in your state and considering your individual needs, you can make informed decisions to ensure adequate coverage. Remember, driving without sufficient insurance can lead to significant financial and legal consequences. Always prioritize safety and financial protection by securing the appropriate level of auto insurance.

Detailed FAQs

What happens if I get into an accident and don’t have enough insurance coverage?

You could be held personally liable for damages beyond your policy limits, potentially facing significant financial losses and legal action.

Can I choose to have more coverage than the minimum required by my state?

Yes, you can choose to purchase higher coverage limits, providing greater financial protection in the event of an accident.

How often should I review my auto insurance policy?

It’s recommended to review your policy annually, or more frequently if there are significant changes in your driving habits, vehicle, or financial situation.

What are some resources for finding additional information about auto insurance minimums?

You can consult your state’s Department of Motor Vehicles website, insurance companies, and consumer protection organizations for reliable information.